" height="21.95706114703747px" id="qM5sFNDIS" transform="translate(3.459 1.023)" width="17.081538493872166px"/></svg>)

" height="16.041644077985946px" id="vPwWmgEb7" transform="translate(2.375 4.207)" width="19.249983003077222px"/></svg>)

" width="20px"><path d="M 0 20 L 0 0 L 20 0 L 20 20 Z" fill="transparent" height="20px" id="Iu2kCeaUT" width="20px"/><path d="M 4.531 6.206 L 0.253 6.206 L 0.253 19.08 L 4.531 19.08 Z M 2.393 4.449 C 3.884 4.449 4.813 3.46 4.813 2.224 C 4.785 0.961 3.884 0 2.421 0 C 0.957 0 0 0.961 0 2.224 C 0 3.46 0.929 4.449 2.364 4.449 Z M 11.178 19.08 L 11.178 11.89 C 11.178 11.506 11.206 11.121 11.319 10.847 C 11.628 10.077 12.333 9.281 13.515 9.281 C 15.063 9.281 15.682 10.462 15.682 12.193 L 15.682 19.08 L 19.961 19.08 L 19.961 11.698 C 19.961 7.744 17.85 5.904 15.034 5.904 C 12.765 5.904 11.747 7.152 11.178 8.029 L 11.178 6.206 L 6.899 6.206 C 6.956 7.414 6.899 19.08 6.899 19.08 Z" fill="rgb(0, 0, 0)" height="19.079659942779543px" id="hzLTqQuQE" transform="translate(0.02 0.461)" width="19.960870207061767px"/></g></svg>)

" height="18px" id="TrPl6m2Z8" transform="translate(1.75 3)" width="20.5px"/></svg>)

Key Takeaways (TL;DR):

Hidden Costs: Advertised rates of 2.9% + $0.30 often mask a realized cost of 4–6% due to currency conversion, cross-border surcharges, and platform fees.

Conversion vs. Fees: For low-ticket items, choosing an embedded checkout that reduces user friction is often more profitable than finding the lowest transaction fee, as it can increase conversion by 40–60%.

Liquidity Factors: Payout timing varies significantly between processors (from instant to 7+ days), which can create critical cash flow gaps for creator businesses with tight margins.

Dispute Management: Chargebacks represent both a direct financial loss and a systemic risk; using recognizable merchant descriptors and automated evidence submission is vital for protecting account health.

Operational Alignment: Successful monetization requires synchronizing payment logic with marketing attribution and subscription mechanics to avoid double-billing, manual reconciliation, and 'attribution blindness.'

Why the advertised rate is only the first ledger line in creator payment processing

Most creators begin vetting a payment processor by looking at a single number: 2.9% + $0.30 per transaction. It's visible. It's simple. It feels comparable. But for a creator trying to accept payments as creator, that advertised rate is a bookkeeping illusion unless you expand the ledger. The full cost picture contains routing fees, cross-border spreads, card network assessments, payout fees, chargeback expense, platform surcharges, and—crucially—conversion losses caused by user experience.

Think of the advertised rate as the headline; everything else is the fine print that actually eats your margin. The headline rarely includes the incremental items that shift a 2.9% headline into a 4–6% realized cost on average. Those increments matter more at scale, and they matter earlier for creators whose per-sale ticket is low and whose cash flow is tight.

Below, I unpack the primary invisible cost drivers and show why your choice of payment processor for creators is a strategic decision, not a product procurement checkbox.

Where fees multiply: the anatomy of actual per-sale cost

Advertised interchange rates are only part of the story. The next layers are operational and behavioral:

- Currency conversion and foreign-exchange spreads. If your buyer's card is billed in a foreign currency, processors often apply a currency conversion fee on top of the card network's FX rate. That spread can add a percentage point or more per transaction.

- Cross-border fees. Some processors apply a cross-border surcharge when the card's issuing country differs from your settlement country.

- Chargeback and dispute worst-case cost. Chargebacks carry a direct fee (often $15–$25) and the lost merchandise or service revenue. Repeated disputes can push merchant risk into higher pricing tiers.

- Platform or marketplace fees. Creator-focused platforms sometimes add a percentage cut or flat fee for marketplace services. That is separate from payment-processing charges and often non-negotiable when you depend on the platform's distribution.

- Settlements, currency conversions at payout, and receivable timing. Some processors hold funds for risk reasons or batch payouts, which increases working capital requirements and can create liquidity shortfalls.

Those items interact. Currency conversion cost compounds with platform fees. Chargebacks not only cost money directly; they also raise your risk profile, increasing reserve requirements or triggering rolling reserves that hold funds back for weeks. For creators with single-digit-dollar items—tips, micro-products—these additions turn a profitable micro-transaction into a loss.

Fee element | Advertised visibility | Typical effect on a $10 sale | Why creators miss it |

|---|---|---|---|

Interchange + processor markup | Visible | ~$0.59 (2.9%+ $0.30) | It's the first and loudest line; everything else seems secondary |

Currency conversion / FX spread | Often hidden | +$0.10–$0.30 (depends on currency) | People assume market FX rate is used |

Cross-border surcharge | Sometimes visible | +$0.10–$0.40 | Unclear when it applies; depends on card issuing country |

Platform fee (creator-specific) | Visible on contract | +$0.20–$1.00 | Creators accept platform reach without modeling margin |

Chargeback cost (expected per-sale) | Not pro-rated publicly | +$0.05–$0.20 expected value | Low frequency makes it feel remote; it accumulates |

The numbers above are qualitative bands, not guarantees. But the pattern is consistent: you often pay materially more than the headline number, and the incremental costs are variable and sometimes opaque.

Payment method support and international routing: where cost and conversion collide

Accepting payments as creator increasingly means supporting more than just card payments. Digital wallets, bank debits, buy now pay later (BNPL), and local payment methods (e.g., SEPA, UPI) matter—particularly for international audiences. Each method has different economics, failure rates, and user flow implications.

Card payments are generally more expensive but convert reliably in many markets. Local rails can be cheaper but often require more integration and present a higher failure rate during first-time setup. Digital wallets (Apple Pay, Google Pay) reduce friction and can lower fraud rates, but they still route through card rails with associated interchange fees.

Routing choices—how the processor handles authorization, whether it tokenizes locally, how it treats 3-D Secure—affect conversion. A processor that forces a full-page redirect for a local payment method increases abandonment risk. A provider that supports in-context wallet flows reduces friction and fraud simultaneously.

International routing brings hidden spreads. When your settlement currency differs from the card currency you face either an FX spread or a requirement to maintain multi-currency accounts. Those arrangements affect both your net revenue and reporting complexity. Creators selling globally should budget for extra operational cost and expect variability month to month.

Subscription mechanics and payouts: cash flow is the operating system for creators

For creators building predictable revenue—subscriptions, membership tiers, recurring micro-payments—the nominal support for recurring billing is only the start. Recurring billing has three operational dimensions you must evaluate: dunning and retry logic, proration and upgrade/downgrade handling, and payout timing relative to churn.

Dunning behavior is critical. When a card declines, what does your processor or billing tool do? Some processors provide automated retry schedules and localized messaging; others leave it to you. If retries are handled externally you may miss the subtle data signals that indicate a customer is at risk, leading to higher involuntary churn.

Proration and plan changes are where bookkeeping breaks: mismatched proration rules between your product layer and the payment processor result in credit notes, manual reconciliation, or billing disputes. Creators often patch this by issuing refunds or one-off invoices—manual work that eats margin.

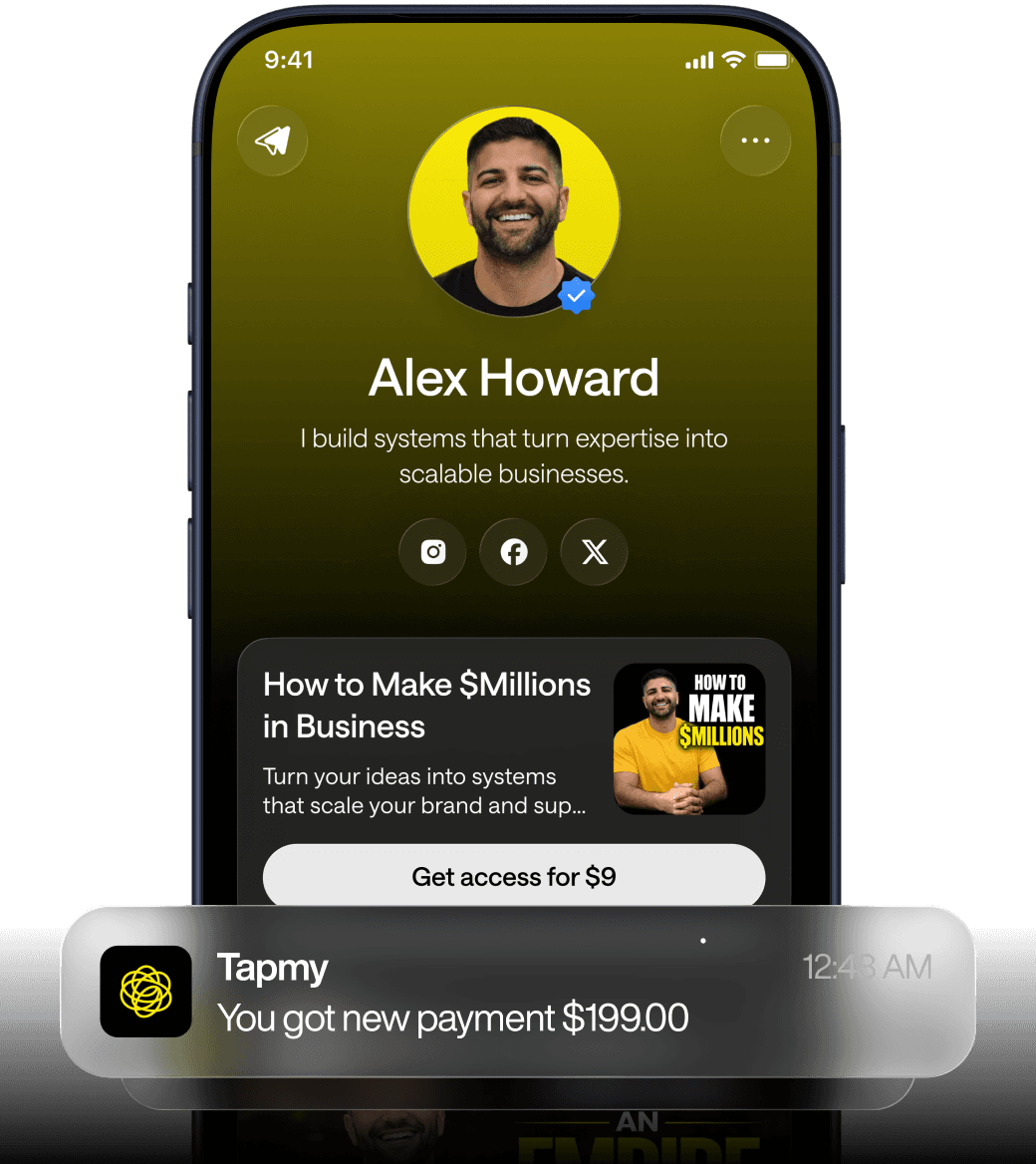

Payout timing directly affects operating liquidity. Some processors (Stripe Instant Payouts, third-party card acquirers) enable near-instant settlement for a fee. Others (PayPal standard settlement) take a few days. Some creator-specific platforms hold funds longer—7 days or more—often for marketplace risk reasons. When you depend on subscription revenue to pay contributors, host events, or buy inventory, a lagging payout schedule triggers short-term cash crunches and forces stopgap borrowings or delayed supplier payments.

Capability | Why it matters operationally | Common creator pain |

|---|---|---|

Dunning automation | Reduces involuntary churn and preserves revenue | Manual retries or no retries cause avoidable losses |

Proration rules | Ensures predictable revenue when plans change | Mismatched proration → refund headaches |

Payout timing | Determines working capital needs | Slow payouts force lines of credit or delayed operations |

Understanding the rhythm of money—authorization timing, settlement, reserve holds and holds release cadence—is essential. Two systems can produce identical revenue on paper but substantially different free cash flow available to run the creator business.

Chargebacks and disputes: a failure mode that scales unpredictably

Chargebacks are not just an expense; they are a systemic risk that can change how a payment processor treats your account. If your dispute ratio crosses platform thresholds, you can be placed on hold, required to post reserves, or shifted to an acquirer with higher fees. Creators with volatile sales patterns or high-ticket offers feel this faster than large merchants.

Common failures that lead to disputes in creator contexts:

- Unclear product descriptions. If a buyer can't reconcile what they paid for with the listed deliverable, disputes rise.

- Unfamiliar descriptor on a bank statement. If the merchant descriptor is the platform rather than your brand (a frequent byproduct of using marketplace payment flows), buyers don’t recognize the charge and dispute it.

- Complex subscription changes. Customers contest charges when proration or refunds were handled poorly.

Handling disputes effectively requires operational tooling: evidence collection, automated descriptor customization, and a post-purchase communication cadence. The first 30 minutes after a dispute notification are often decisive; automated evidence submission reduces the win-loss variability. Many creators discover too late that their chosen payment processor either doesn’t support rich evidence uploads or requires manual processes that are slow and error-prone.

There's also a behavioral component. Disputes cluster around edge-case customer experiences—long delivery times, ambiguous access controls, or complicated cancellation paths. Fix the customer experience, and disputes decline. Fixing the customer experience, however, often requires product and billing changes that span your monetization layer and payment processor—hence the relevance of an integrated attribution that connects attribution to buys and support.

Integration choices: embedded checkout vs external redirect and the conversion trade-off

One of the most consequential integration choices for creators is whether to use embedded payment processing (checkout that stays on your branded page) or an external checkout that redirects users to a processor's hosted page. The trade-offs are straightforward in theory but messy in practice.

Embedded checkout pros: better conversion, more control over UI/UX, consistent branding, and richer first-party data capture. Embedded flows reduce friction and let you attach content attribution to purchases at the moment of sale. That attribution matters when you want to know which video, post, or newsletter drove the payment.

External checkout pros: lower integration effort, less PCI surface to manage, and sometimes faster time to market. Hosted pages offload compliance and tokenization, which is attractive for creators without developer resources.

Conversion differences are material. Industry observations place embedded checkout conversion uplift at roughly 40–60% higher than external redirects. That range isn't a guarantee but does reflect a consistent pattern: keeping the buyer on your page reduces context switching and trust friction. For low-ticket items, that uplift dwarfs small differences in per-transaction fees.

But embedded means responsibility. You need tokenization, session continuity, proper PCI handling (or a vaulting provider), and a UX that degrades cleanly when the card declines or 3-D Secure kicks in. If implemented poorly, an embedded flow can raise friction at precisely the moment you were trying to reduce it.

Below is a decision matrix that distills when embedded or external checkout is the better fit for creators, emphasizing the trade-offs rather than prescribing a single path.

Scenario | Embedded checkout | External/hosted checkout |

|---|---|---|

Low-ticket, high-volume items (tips, micro-donations) | Preferred — conversion uplift matters most | Acceptable if integration resources are zero |

Occasional high-ticket sales (coaching sessions) | Beneficial for brand trust and cross-sell attribution | Works if you need rapid deployment and dispute handling |

Complex subscriptions with proration | Better — allows consistent UI for upgrades/downgrades | Riskier — hard to reconcile behavior across two systems |

Limited dev resources | Requires investment or third-party embedded solutions | Fastest path; lower maintenance |

One practical pattern I’ve seen work: start with hosted checkout to validate demand; then migrate to embedded checkout for recurring revenue and micro-transactions where conversion uplift justifies the engineering cost. Migration costs are real. You need migration plans for subscription tokens, webhook handling, and your reporting layer. Vendors differ wildly in how they support that migration; compare their token portability and webhook reliability before you commit.

Platform comparisons: how Stripe, PayPal, Square and creator-specific platforms differ in practice

Comparisons in marketing collateral and on a product feature grid make everything look clean. Reality is messier. Below is a qualitative comparison that highlights practical differences you should expect when selecting a payment processor for creators.

Processor | Advertised rate | Typical actual cost (common additions) | Payout speed (examples) | Creator-specific strengths |

|---|---|---|---|---|

Stripe | ~2.9% + $0.30 (US card) | +FX spreads, cross-border fees, dispute fees → often 4–5% effective | Instant payouts available for a fee; standard 1–2 days | Strong API, good subscription tooling, robust webhooks |

PayPal | ~2.9% + $0.30 (varies by sale type) | +currency conversion spreads, cross-border fees; platform fees if using PayPal Commerce | Standard ~3 days (varies by region); instant options exist | Buyer trust, strong in-person and wallet flows |

Square | ~2.9% + $0.30 (online) | +chargeback fees, currency effects for international | Typically next-business-day settlements for many sellers | Simple bundled hardware + payments for creators who sell IRL |

Creator-specific platforms | Varies; often includes platform fee + underlying processor fee | Platform fee plus payment processing → can be 4–6% or higher total | Some hold funds 7+ days; others pass-through faster | Built-in community features, subscription management, and discoverability |

Two practical takeaways from the table: first, the advertised rate compresses variance and hides critical decision variables like payout timing and platform fees. Second, capability matters: Stripe’s API flexibility makes it easier to build attribution into your billing, while creator-specific platforms may offer features you can't replicate quickly but at the cost of fees and data lock-in.

What breaks in real usage: common failure patterns and how they manifest

Real projects don't fail from single points of friction. They fail from the accumulation of mismatches between product behavior, payment logic, and customer expectations. Here are concrete failure patterns I've seen repeatedly when creators try to scale payments.

1) Disconnected attribution and fragmented reporting — symptom: you can't tell which newsletter or clip generated a sale without manual reconciliation. Cause: using a marketplace or external checkout that handles auth and settlement separately from your content attribution system. Consequence: poor promotional ROI decisions and missed opportunities to scale what works.

2) Subscription mismatch failure — symptom: customers get double-billed or lose access after plan changes. Cause: proration implemented one way in the product layer and another in the processor; webhooks missed or handled out of order. Consequence: refunds, disputes, and customer churn.

3) Liquidity shocks from payout lag — symptom: you can't pay collaborators or run an event because funds are delayed. Cause: platforms that impose multi-day holding periods or reserve policies during spikes. Consequence: operational freezes and reputational damage.

4) Increased disputes due to unfamiliar descriptors — symptom: sudden uptick in chargebacks from buyers who don't recognize the merchant name. Cause: platform-level descriptor or shared acquirer names. Consequence: higher fees and tighter underwriting.

5) Poor UX in 3-D Secure flows — symptom: checkout abandonment when banks require authentication. Cause: poorly implemented authentication flow or full-page redirects that interrupt the purchase. Consequence: high abandonment precisely during peak fraud-protection events (often around big sales).

Fixing these requires a combination of engineering, policy, and merchant-config changes. Sometimes the fix is architectural (move to embedded checkout). Sometimes it's operational (change descriptor text and customer notification cadence). Rarely is a single vendor swap sufficient; more often you need coordinated changes across your monetization layer: attribution, offers, funnel logic, and repeat revenue controls. See role of attribution for deeper guidance on closing the loop between content and payments.

Decision matrix: choosing a payment processor for creators with constraints and trade-offs

Below is a compact decision matrix focused on the trade-offs that matter to creators who are overwhelmed by choices. It is not exhaustive but should help you prioritize which dimensions you must evaluate based on your business model.

Primary need | Key trade-off | Recommended processor traits |

|---|---|---|

Maximize conversion on low-ticket items | Investment in embedded checkout vs short-term speed | Support for embedded flows, wallet tokens, and fast auth (3-D Secure handling) |

Minimize operational overhead | Hosted checkout reduces complexity but lowers control | Hosted pages with reliable webhooks and clear settlement timing |

Global audience | Card coverage vs local payment support and FX handling | Multi-currency settlement, local rails support, transparent FX pricing |

Subscription-first business | Dunning and proration complexity | Rich subscription tooling, automated dunning, clear proration rules |

Attribution and monetization analytics | Keeping payment data together with content attribution | Embedded payment support plus first-party attribution capture (monetization layer) |

Two important notes: first, prioritize the dimension that most tightly constrains your economics (conversion, payout timing, or fee escalation). Second, insist on testing before committing. Run a 2–4 week A/B on checkout experience or simulate subscription churn scenarios to observe dunning performance. Vendors will promise performance; you need measured signals.

Reconciling the accounting and the customer data: an operational anti-pattern

Many creators adopt a 'best-of-breed' approach: a payments provider here, a subscription manager there, an analytics tool elsewhere. It sounds sensible, but in practice this creates three operational pathologies:

- Manual reconciliation. When settlement reports come from different systems, you spend significant time matching transaction IDs, webhooks, and payouts. That's work with low marginal value.

- Attribution blindness. Without a single record that ties content, campaign, and payment, you make promotional decisions with noisy data. You might double down on a tactic that looks good in one system but underperforms when payment friction is included.

- Fragmented customer experience. Support teams need to chase records across systems to resolve refunds or access issues, extending resolution times and increasing dispute risk.

There is no universal remedy. But the conceptual framing matters: treat your monetization layer as attribution + offers + funnel logic + repeat revenue. If your payment architecture separates these concerns into disconnected systems, you lose the ability to optimize holistically. Integration is less about APIs and more about closing the loop: who gets credit for a sale, how that sale changes the user's entitlements, and how refunds/chargebacks are routed back into attribution and product decisions.

Practical checklist for creators ready to accept payments

Here is a compact checklist that shifts the conversation from product features to operational outcomes:

- Map your price points and expected average order value (AOV). Low AOV increases the importance of conversion uplift relative to per-transaction fee differences.

- Define your settlement needs. Do you require same-day liquidity, or can you tolerate multi-day holds? If you need fast cash flow, prioritize payout options and associated costs.

- Choose payment methods aligned with your geography. If 30–40% of your audience is outside your country, support local rails or multi-currency settlement to reduce FX drag.

- Evaluate dispute processes end-to-end. Confirm how evidence is submitted, whether descriptors can be customized, and how the processor treats subscription disputes.

- Test checkout flows in-market. Run a short experiment comparing embedded vs hosted checkout on your actual product pages.

- Plan for reconciliation. Decide whether you will centralize settlement reports into your accounting system or accept manual reconciliation as a recurring cost.

FAQ

How should I weigh per-transaction fees versus conversion uplift when choosing a payment processor?

It depends mostly on your average order value and purchase frequency. For low-AOV items, small gains in conversion from embedded checkout typically produce more incremental revenue than cutting a few basis points off fees. For high-AOV, infrequent purchases, the per-transaction fee becomes more significant. Run a simple sensitivity model: multiply expected lift in conversion by traffic volume and average order value, then compare against the incremental fee cost. The outcome usually favors conversion for small-ticket items and fee optimization for large-ticket sales.

Are creator-specific platforms worth the higher aggregate fees?

They can be, but only when the platform's audience or tooling materially replaces what you'd otherwise have to build or buy. Creator platforms bundle discoverability, subscription plumbing, and community features that accelerate go-to-market. The trade-off is data lock-in, platform fees, and potentially slower payouts. If you rely on precise attribution and want full control over customer relationships, the extra fee can be costly long-term. Evaluate by modeling the incremental revenue the platform brings versus the total fees it charges.

What is the practical impact of payout timing—how tight will my cash flow become?

Payout timing affects liquidity, not net profit. If you operate on thin margins or pay contributors in short windows, a 3–7 day payout lag can force borrowing or canceled plans. Also consider reserve policies: sudden spikes in sales often trigger temporary holds. Plan buffer cash or negotiate advance payout terms if you need reliable short-term liquidity. If you can, test payout timing during your high-volume moments before committing to a long-term arrangement.

Can hosted payment pages protect me from PCI and fraud exposure fully?

Hosted pages reduce your PCI surface because sensitive card data is never handled by your servers. They also offload some fraud-handling responsibilities. But they don't eliminate the need for secure webhooks, signed callbacks, and robust reconciliation. Moreover, hosted pages can still increase chargebacks if they use generic descriptors or create confusion for buyers. Treat hosted pages as partial mitigation, not a full substitute for thoughtful fraud policy and clear buyer communications.

How should I handle disputes that originate from subscription misunderstandings?

Design for clarity. Provide clear subscription descriptors, send immediate post-purchase emails that show the billing cadence, and include an easy, visible cancellation flow. Operationally, capture evidence of access and communications tied to the subscription event; store it where it can be attached to the dispute. If your payment processor supports automated evidence submission, enable it. Finally, analyze dispute themes periodically—if a significant share are subscription misunderstandings, revise your product copy and initial onboarding.