" height="21.95706114703747px" id="qM5sFNDIS" transform="translate(3.459 1.023)" width="17.081538493872166px"/></svg>)

" height="16.041644077985946px" id="vPwWmgEb7" transform="translate(2.375 4.207)" width="19.249983003077222px"/></svg>)

" width="20px"><path d="M 0 20 L 0 0 L 20 0 L 20 20 Z" fill="transparent" height="20px" id="Iu2kCeaUT" width="20px"/><path d="M 4.531 6.206 L 0.253 6.206 L 0.253 19.08 L 4.531 19.08 Z M 2.393 4.449 C 3.884 4.449 4.813 3.46 4.813 2.224 C 4.785 0.961 3.884 0 2.421 0 C 0.957 0 0 0.961 0 2.224 C 0 3.46 0.929 4.449 2.364 4.449 Z M 11.178 19.08 L 11.178 11.89 C 11.178 11.506 11.206 11.121 11.319 10.847 C 11.628 10.077 12.333 9.281 13.515 9.281 C 15.063 9.281 15.682 10.462 15.682 12.193 L 15.682 19.08 L 19.961 19.08 L 19.961 11.698 C 19.961 7.744 17.85 5.904 15.034 5.904 C 12.765 5.904 11.747 7.152 11.178 8.029 L 11.178 6.206 L 6.899 6.206 C 6.956 7.414 6.899 19.08 6.899 19.08 Z" fill="rgb(0, 0, 0)" height="19.079659942779543px" id="hzLTqQuQE" transform="translate(0.02 0.461)" width="19.960870207061767px"/></g></svg>)

" height="18px" id="TrPl6m2Z8" transform="translate(1.75 3)" width="20.5px"/></svg>)

Key Takeaways (TL;DR):

Conversion Advantage: Integrated single-page checkouts see approximately 28% abandonment compared to 73% for external redirects, primarily by eliminating 'context switching' and 'trust leakage.'

Implementation Styles: Creators can choose between client-side SDKs (like Stripe Elements) for high control or platform-native abstractions that handle PCI compliance and technical complexity.

Fulfillment Automation: Simply adding a button is insufficient; creators must implement robust backend logic for digital delivery, subscription dunning, and inventory locks to avoid 'race conditions.'

Mobile Optimization: Success on mobile depends on supporting platform wallets (Apple/Google Pay) and using progressive disclosure to minimize form fields in restrictive in-app browsers.

Operational Risks: Key failure modes include payment SDK incompatibilities in social app webviews, regional currency mismatches, and complex international tax (VAT) obligations.

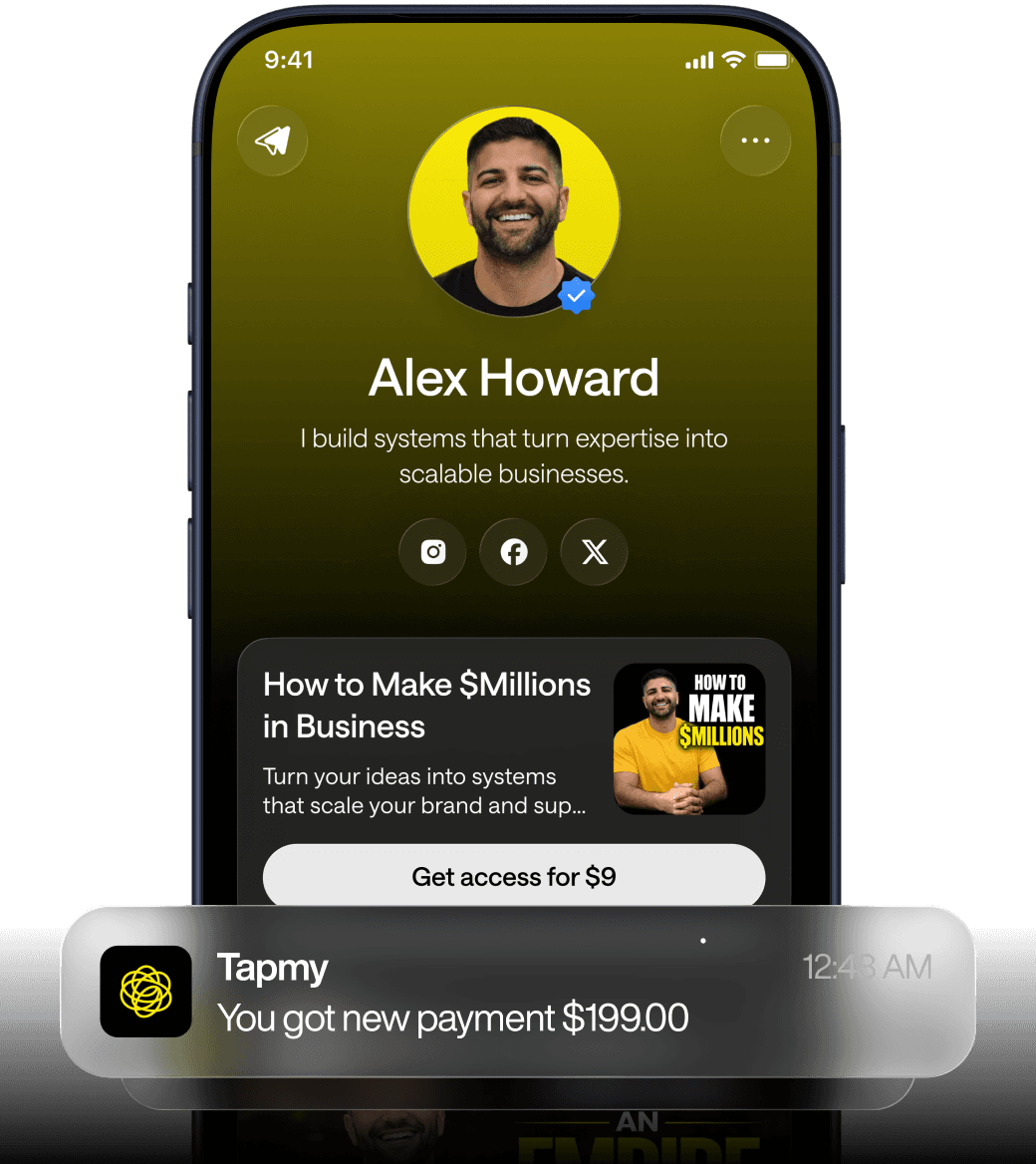

Why reducing redirect friction from five steps to one changes user behavior

Most creators who redirect buyers out of the social app assume navigation is the only cost. It's not. Every extra step multiplies friction: cognitive load, perceived risk, and the chance the customer gets interrupted. When a buyer taps a "Buy" button on a bio link and is bounced to a multi-page external checkout, the experience often includes a browser switch, a new UI, and one or more unfamiliar forms asking for the same information they already gave. The cumulative effect is predictable — abandonment.

Two behavioral mechanisms are at work. First, attention leakage: switching contexts (in-app → external browser → external merchant) breaks the short-term memory chain that held intent together. Second, trust leakage: unfamiliar layouts and third-party domains increase perceived risk, which triggers hesitation or a search for reviews and alternatives. Both phenomena operate at sub-second and multi-minute timescales. A lost micro-moment compounds into a lost sale. If you rely on a social app audience without optimizing the post-click flow, you'll see this exact pattern.

Quantitatively, practitioners observe a large gap in abandonment rates between multi-step external checkouts and single-page native checkouts embedded in the bio link. The friction analysis often cited — roughly 73% abandonment with external redirects versus about 28% with integrated single-page checkout — points to how much of conversion is pure flow design, not product-market fit. That margin isn't guaranteed; it's conditional on execution quality: form length, trust signals, payment method familiarity, and mobile performance.

Why does a single in-bio checkout convert more? It removes the context switch, preserves the referral signal (no drop of UTM attribution), and maintains the user's mental model: the buyer clicked in the social app, they purchase in the same environment. Small cues—same typography, immediate product confirmation, a single scroll—reduce friction in ways analytics can measure (lower time-on-page, fewer pages per session) and in ways they can't (reduced hesitation before hitting the final CTA).

How embedded in-bio payment flows are implemented: what actually happens under the hood

There are two broad architectures for payments inside a bio link: client-rendered in-page checkout that talks to a payment gateway via tokenization, and redirect-based flows where the user is sent to the processor's hosted UI. The first is what people mean when they say "native" — the checkout appears to live where the product link lives. The second is a handoff. Both are legitimate, but their failure modes and constraints differ. If you need a deeper primer on choosing a platform, see link-in-bio platform options.

In a client-rendered flow, the page collects payment details using a payment SDK (for example, a Stripe Elements or a PayPal JS SDK). Card data never lands on your servers; it's sent to the processor's tokenization endpoint which returns a short-lived token. Your application attaches that token to an order and submits it to your backend. The backend confirms the charge with the processor and fires fulfillment webhooks.

Those tokenization steps are the critical safety valve: they reduce your PCI scope and let the processor handle sensitive fields. But there are practical constraints: some webviews (for example, older in-app browsers) limit JavaScript features or block third-party cookies; that breaks some SDKs. Apple Pay/Google Pay use platform-level wallets and require additional handshake steps (merchant validation for Apple Pay, for instance). Getting those specifics right is a frequent operational task.

Stripe, PayPal, and platform-native systems differ in how they expose tokenization, webhooks, and hosted pages. Stripe emphasizes flexible client SDKs and strong webhook primitives. PayPal offers both hosted checkout buttons and JS SDKs, but historically pushes users toward their hosted pages. Platform-native systems (the ones embedded into a link-in-bio product) can abstract the processor entirely so the buyer perceives a single-page flow while the backend uses one or more processors for settlement.

Dimension | Stripe-style (SDK + tokens) | PayPal-style (hosted + SDK) | Platform-native (abstracted checkout) |

|---|---|---|---|

Frontend integration | Client SDK, Elements, custom UI | JS button or redirect; hosted option common | Single embedded UI; platform manages processor |

PCI scope | Low if using Elements / tokenization | Low with hosted; moderate with full SDK | Lowest for creator; platform handles compliance |

Control over UX | High | Moderate | High for creator but within platform constraints |

Failure points | SDK compatibility, webview limitations | Unexpected redirects, cross-domain issues | Platform outages, misconfigurations |

Note: the table describes qualitative trade-offs; it isn't exhaustive. Production systems often mix approaches: a platform-native UI that uses Stripe on the backend, or an SDK that falls back to a hosted page when a webview blocks required features.

Product types that work (and the downstream automation patterns they require)

Not every product behaves the same when you move checkout into a single-page bio link. The payment model defines the fulfillment logic. A one-time digital download needs a signed download link and a delivery email. A subscription requires billing cycles, proration rules, and a mechanism to handle card updates. A booking needs real-time availability checks and calendars. Tips and donations may not need fulfillment but still need receipts and tax classification. Recognize the variance early; mixing models under a single checkout widget increases complexity.

For each product type, specific automation patterns are common:

Digital goods: generate a unique, expiring download URL or license key after confirmation. Automate delivery with a webhook that triggers email and stores the key in a CRM.

Subscriptions: create the subscription object at the processor, map plan IDs, set trial periods, and decide who handles proration when customers change tiers. Watch for failed subscription renewal handling — retries and dunning sequences are essential. See best practices for Subscriptions.

Bookings: integrate a read-through availability check at checkout to prevent double-booking. Use pessimistic locking on inventory when steps are asynchronous; otherwise double sells happen.

Tips/donations: reveal any platform fees and tax treatment up front. If payments are pooled and paid out later, manage liability and disclosures carefully.

What creators try | What breaks in practice | Why it breaks |

|---|---|---|

Send a download link immediately after charge without token checks | Stolen links, link sharing, chargeback vulnerability | No unique tokenization; lack of authenticated access |

Create subscriptions without a dunning process | Recurring revenue drops, unpaid invoices accumulate | No automated retries or customer-facing payment update flow |

Reserve booking only after payment confirmation | Competing buyers pay at the same time; double booking | Race conditions; absence of temporary hold or inventory lock |

The takeaway: when you add payments to a bio link, you are not just adding a button. You are attaching a fulfillment contract to that button. Fulfillment needs automation primitives: webhooks, retries, inventory locks, and idempotent order handling. If you skip those primitives and rely on manual fulfillment, disputes and negative reviews will follow. For more on building the underlying system, review how to build a scalable monetization system.

Common failure modes: what breaks in real usage and how to detect it

Expect breakage. Real-world systems fail in predictable ways. Below I list several failure modes and the underlying root causes so you can design monitoring and mitigation.

1) Payment SDK incompatibility in social app webviews. Root cause: some in-app browsers block third-party cookies or prevent certain JS features. Symptom: payment form fails to render or tokenization requests time out. Detection: synthetic tests using the same in-app user agent and monitoring for JS exceptions. If you need a checklist for common integration mistakes, see Common failure modes.

2) Currency and region mismatch. Root cause: the buyer sees product prices in their locale but the processor settlement currency differs, or the product isn't available in the purchaser's country. Symptom: charge declined or flagged for additional verification. Detection: monitor decline codes and map them to geography; expose region-specific UI messaging.

3) Incomplete tax handling, specifically VAT and digital goods. Root cause: incorrect tax calculation for local rules, or omission of required invoice details. Symptom: refunded charges due to tax authority complications or customer complaints. Detection: audit orders for tax line presence; sample cross-border transactions monthly.

4) Fulfillment race conditions. Root cause: creating fulfillment records before confirmation that the charge succeeded (or vice versa). Symptom: customers receiving goods without payment, or not receiving goods despite successful charge. Detection: reconcile payment events with fulfillment events using unique order IDs; alert on mismatches.

5) Chargebacks and disputes handled on platform rather than with the processor. Root cause: ambiguous liability boundaries between creator and platform. Symptom: delayed response to disputes, higher dispute loss rates. Detection: track dispute response timelines and ownership clarity in the platform policy.

Assumption | Reality | Operational implication |

|---|---|---|

"Hosted checkout will always work in-app" | Some hosted flows redirect and break inside webviews | Provide SDK fallback or a compact modal-based checkout |

"One payment method is enough" | Buyers prefer platform wallets (Apple/Google Pay) on mobile | Support wallets to reduce friction and declines |

"Processor handles taxes" | Processor may assist but creator remains responsible | Integrate tax calculation or require sellers to configure tax rules |

Detection and monitoring are the pragmatic first defenses. Instrument tokenization endpoints, webhook delivery, and dispute events. Alert on unexpected decline trends. Set up synthetic purchases in different geographies and user agents to catch webview regressions before they affect customers. If you're evaluating platforms, a deep dive on link-in-bio platform capabilities will save time.

Mobile checkout patterns that reduce abandonment and their trade-offs

Your mobile UX choices are decisive. Small improvements produce outsized outcomes because mobile sessions are short and error-intolerant. I list practical patterns, why they work, and the trade-offs involved.

One-click purchases and saved payment methods. Why: reduces number of form fields and removes re-entry friction. How: tokenize a card at first payment and reuse the token for future purchases, taking care with consent and vaulting rules. Trade-offs: storing tokens requires clear privacy language and the proper consent flow. For subscriptions, token reuse must be tied to the subscription object at the processor.

Platform wallets (Apple Pay, Google Pay). Why: instant authentication, autofill of card and address reduces abandonment drastically on iOS and Android. How: implement merchant validation and present the wallet button in the first view. Trade-offs: wallets are not globally ubiquitous (Apple Pay availability varies by region and device), and the integration requires domain verification and sometimes specific certificate handling.

Progressive disclosure of fields. Why: reduce initial friction by asking only for essentials; reveal additional fields only if needed. How: use inline validation and optional modals for non-critical fields. Trade-offs: additional client complexity, potential confusion if the flow reveals fields mid-process. Test with real users.

Explicit trust signals. Why: they offset perceived risk when buyers haven't left the social app. How: show SSL, processor badges, transparent refund policies, and order previews. Trade-offs: clutter can reduce clarity. Choose a small, consistent set of signals and A/B test placement rather than adding everything. For concrete examples of effective CTAs and placement, consult call-to-action examples.

Decision matrix: when to use native in-bio checkout vs. redirecting to external pages

Not every creator should always aim for a fully embedded checkout. There are constraints — complexity, compliance burden, product model — that make redirects legitimate choices. The matrix below maps common decision factors into a practical recommendation.

Decision factor | Favor embedded in-bio checkout | Favor redirect / hosted checkout |

|---|---|---|

Conversion priority | High — single-page checkout reduces abandonment | Lower — acceptable if conversion is not critical |

Technical resources | Available — backend to process webhooks and automate fulfillment | Limited — prefer hosted pages to offload complexity |

Product complexity | Simple: one-offs, tips, digital downloads, subscriptions | Complex: variable pricing, heavy compliance (KYC), in-app purchases |

Device/browser constraints | Modern webviews and support for wallets | Old or restrictive in-app browsers where SDKs fail |

Regulatory / tax needs | Manageable tax rules with a tax engine | Complex VAT/KYC obligations better handled by a hosted solution |

One practical pattern is hybrid: default to embedded checkout for mobile users with compatible webviews and wallets, but detect problematic contexts and fall back to a hosted page. This balances conversion performance with compatibility, though it increases testing surface. If you're wrestling with platform trade-offs, read our monetization layer breakdown for guidance.

How the "monetization layer" perspective changes integration priorities

Think of payment integration not as a feature toggle but as the monetization layer: attribution + offers + funnel logic + repeat revenue. This framing changes where you invest engineering and product effort.

Attribution: when checkout is embedded, the referral context and UTM parameters remain intact. That matters to campaign ROI calculations and retargeting logic. Lose that when you redirect, and you lose the clean signal.

Offers and funnel logic: embedded checkouts can show contextual offers (a one-click upsell modal, an accommodation for shipping options) with minimal friction. Implanting offers into the same page keeps the conversion funnel short and observable.

Repeat revenue: saved payment methods and subscription management live inside the monetization layer. If you separate checkout into multiple systems, retaining the user's payment preferences and subscription history becomes a synchronization problem. Platform-native checkouts tend to centralize that state.

Operationally, that monolithic view forces trade-offs. Centralizing payments increases the platform's liability (compliance, payout cadence, dispute handling). Platform decentralizing (each creator connects their own Stripe account) reduces platform liability but increases the complexity of onboarding and support. Decide which risk profile matches your operating model.

Compliance, refunds, disputes, and international considerations you must plan for

Payments trigger regulatory and operational obligations. Ignore them and you will face refunds, elevated chargeback rates, or legal exposure.

Refunds and chargebacks: design workflows that reconcile payment processor events with your order system. A good practice is idempotent processing of webhook events; maintain an immutable order log for every payment-related event. When a refund or chargeback occurs, the dispute lifecycle differs by processor; respond promptly and provide clear evidence. Platforms that defer responsibility to creators should make dispute ownership explicit in the interface. For more on operationalizing these responsibilities, see Tax compliance and related guidance.

International payments: currency conversion and region restrictions bite unexpectedly. If you price in a single currency, buyers still pay through their card network, which can trigger foreign transaction fees or currency mismatch declines. Consider a localized pricing strategy when you have repeated sales in specific markets. Also, be aware that payment methods vary by region — wallets popular in one country may be non-existent in another.

Tax compliance: whether it's sales tax, VAT, or GST, you must either collect taxes at checkout or maintain documentation showing tax-exempt status. Processors sometimes offer tax add-ons, but relying on them without understanding local rules is risky. For digital goods, VAT rules can be particularly intricate and vary by buyer location.

Data protection: tokenization reduces your PCI footprint but doesn't eliminate data protection obligations. Order receipts, customer names, and email addresses are personal data under GDPR and similar regimes. Limit retention, provide export/deletion paths, and document your data flows in case of audits.

When native in-bio checkout fails to outperform redirects

Integrated checkout is not a panacea. It fails to deliver better conversion when the implementation is poor or when other factors dominate the buyer's decision. Examples:

Poorly optimized forms. If the in-bio checkout replicates the same long-form fields as an external form, the benefit of remaining in-place disappears. Buyers still drop out at the point of cognitive overload.

Unreliable payment methods. If you support only niche payment methods, you may reduce conversion regardless of embedded UX. Wallets and major card networks matter.

Pricing and value misalignment. If the product-market fit isn't there, faster checkout only accelerates negative outcomes (more refunds, more disputes). Conversion improvements are most valuable when the offer itself is solid.

Platform trust deficits. If buyers distrust the platform or the creator, staying in the app won't fix persuasive problems. Trust is built by reviews, clear policies, and signaling, not technical integration alone. If you're evaluating platform choices under those constraints, our link-in-bio platform guide can help you compare options.

FAQ

How can I reduce PCI compliance burden when I add payments to a bio link?

Use a tokenization-based integration where card data is captured by the payment processor's SDK (for example, Elements or an equivalent). That directs sensitive fields away from your infrastructure, which typically reduces your PCI SAQ level. Still, you must document data flows and ensure that any components that render or trigger the tokenization are secure and up-to-date. If you're on a platform that provides a native checkout, verify who holds responsibility for PCI compliance—platform or creator—and get that in writing.

What are the practical steps to handle failed subscription renewals in an in-bio checkout model?

Implement a dunning strategy: automated retries with spaced intervals, email and in-app notifications that prompt users to update payment details, and a short grace period before access is revoked. Use the processor's webhook events to detect invoice.payment_failed and invoice.payment_succeeded events and make those events drive entitlement decisions. Store metadata on the subscription object so you can trace customer communications and retry attempts.

If a social app's webview blocks my payment SDK, what fallback options work best?

Detect the webview environment at page load and choose a fallback flow. Good fallbacks include a compact hosted checkout page opened in the system browser or a lightweight modal that collects minimal information sufficient to create a payment intent server-side, with a follow-up authorization step. The hybrid approach reduces loss from webview incompatibility but requires careful testing across versions of Instagram, TikTok, and other apps. For tactical ideas on what breaks in practice, review our mistakes guide.

Do saved payment methods or vaulting increase fraud risk for creators?

Vaulting tokens themselves aren't sensitive if managed correctly; they simply reference payment instruments held by the processor. Fraud risk exists when tokens are misused or when the business model invites chargebacks. Mitigate risk with device signals, velocity checks (limiting how many purchases originate from the same token in a short window), and post-purchase monitoring. Ensure you have clear refund and dispute policies visible at checkout to reduce disputes born from expectation mismatch.

How should I think about taxes for small cross-border digital sales through a bio link?

Start by determining where your buyer is located and what local rules apply to your product. For low-volume sellers, configuring a simple tax engine or integrating with tax services often covers most cases. However, EU VAT for digital goods requires attention: you may need to collect VAT at the buyer's rate and retain records. If complexity exceeds your capacity, restrict sales to a few jurisdictions or present gross prices with clear tax handling language until you can operationalize automated tax calculation.